Leading the Way: Male Millennials Shaking Up the Banking Payments Market

A new survey commissioned by personal finance comparison website finder.com and conducted by global research provider Pureprofile has found that young men are leading the way with using digital payment technology to transfer money.

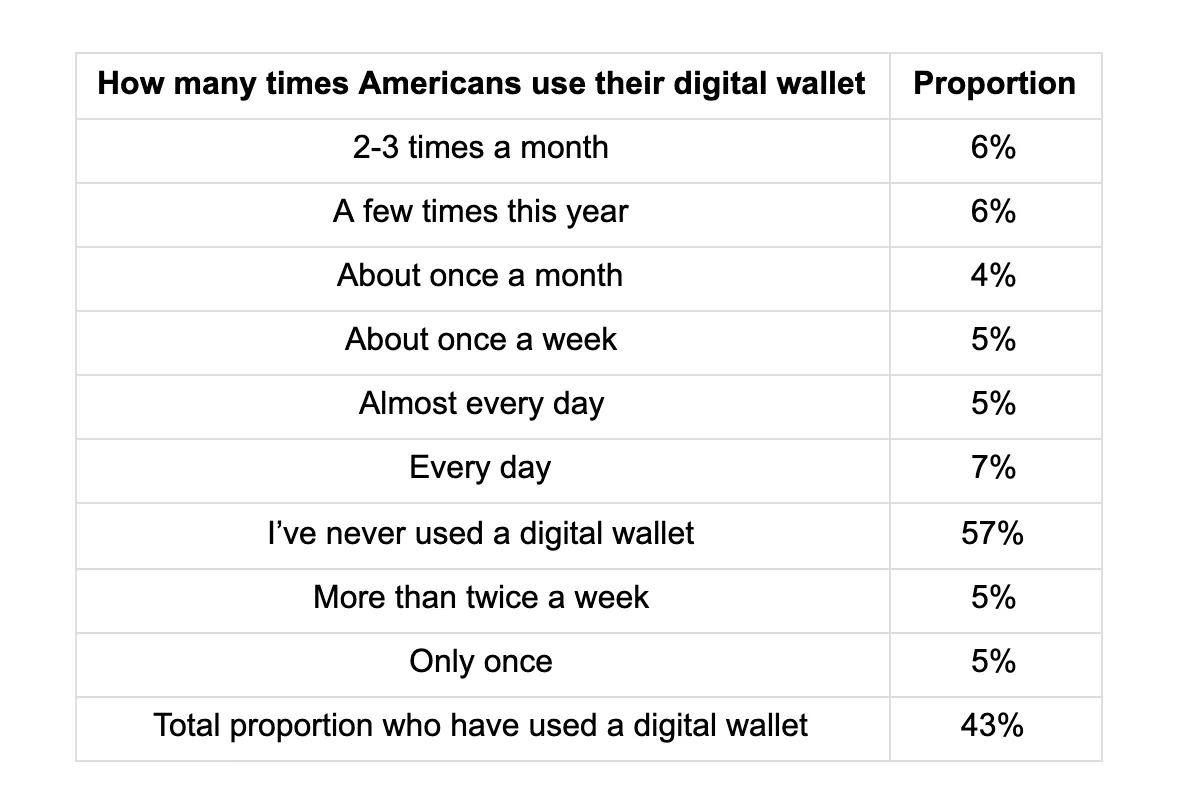

- Over 2 in 5 (43%) of Americans have used a digital wallet to send or receive money this year, such as Venmo, Facebook Messenger, Google Wallet, Apple Passbook, Lemon Wallet, Square Wallet, Chirpify

- That’s an estimated 106.6 million American adults, according to personal finance comparison website finder.com

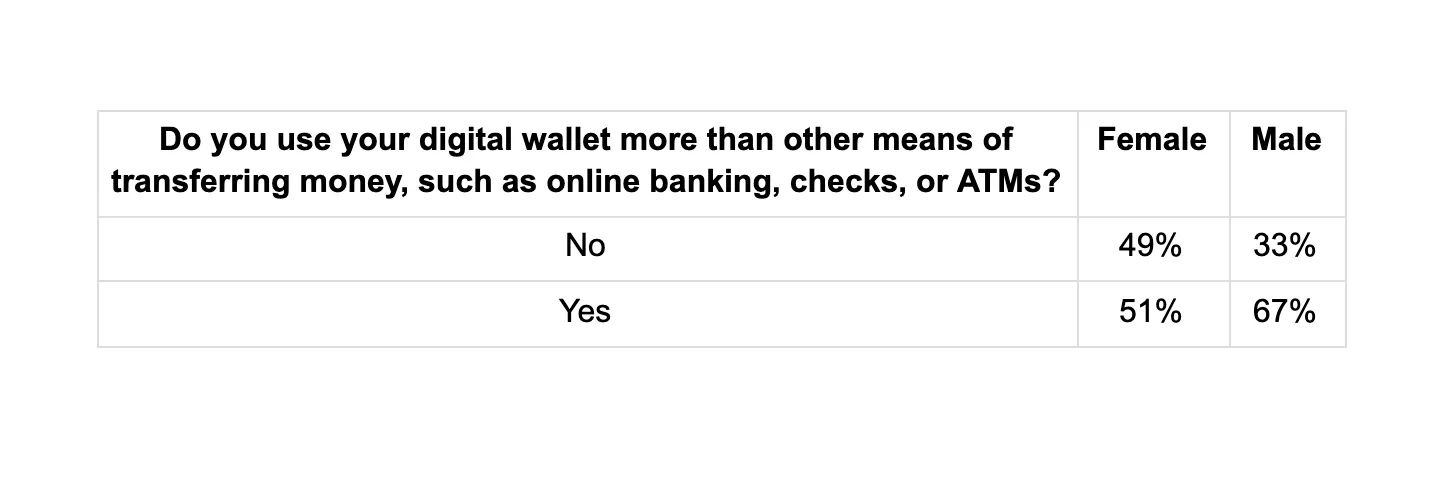

- Interestingly, more than half (57%) of Americans (60.7 million adults) use their digital wallet more than any other means for transferring money, such as online banking, checks, or ATMs

- 31% use their digital wallets at least once a month

- 7% use their digital wallets every day

A new survey commissioned by personal finance comparison website finder.com and conducted by global research provider Pureprofile has found that young men are leading the way with using digital payment technology to transfer money.

Not only are they using them more than other means of transferring money, such as online banking or checks, but they also tend to spend more money when using their digital wallets.

How many times Americans use their digital wallet

Source: finder.com

Gender breakdown

- Men are more likely to use a digital wallet than women, with over half of men (51%) who have used one in the past year, compared to 39% of women.

- Men are also more frequently using their digital wallets, with 41% saying they use it once a month or more, while 27% of women use theirs at least once a month.

- Men are three times more likely to use their digital wallets every day than women (12% versus 4% respectively).

- Men are more likely to spend up than women when using their digital wallets and more likely to use their digital wallets more than other means of transferring money.

Do you use your digital wallet more than other means of transferring money, such as online banking, checks, or ATMs?

Source: finder.com

Generations

- Millennials (18-34) are the biggest users of digital wallets, with 64% using one in the past year – 50% of which use them regularly (at least once a month).

- 40% of Generation X (35-54) have used a digital wallet in the past year, while 17% of Baby Boomers (55+) have done so.

- Millennials are also more likely to spend more than other generations when using their digital wallets and use it more than other ways to transfer money.

Income, education, employment

- The more you earn, the more likely you will use a digital wallet and spend more money. For example, 60% of those who earn over $100,000 have used a digital wallet in the past year – that’s double the proportion of those who earn half as much.

- Those with tertiary education are more likely to use a digital wallet than those who only completed high school.

- Students are the biggest users of digital wallets, with 63% of students taking on the trend, followed by people who work for wages (57%), self-employed (49%), and homemakers (39%)

- Retirees are the least likely to use a digital wallet, with only 17% that have used one, followed by those unable to work (21%) and those out of work (28%).

Ethnicity

- Asian Americans are the biggest users of digital wallets compared to other ethnicities, with 68% saying they have used them in the past year.

- They are followed by Hispanic or Latino (55%) and African Americans (53%).

Marital status

- The biggest digital wallet users according to marital status are singletons who have never married (53%), followed by married/domestic partnership (42%), and those who have separated (35%).

Dependents

- The more kids you have, the more likely you are to use a digital wallet. This is not surprising as digital wallets can be more cost-effective to transfer money than other means.

Comments by Michelle Hutchison, Money Expert at finder.com:

“Most of us carry our phones with us everywhere we go, and new mobile apps make it easier than ever for it to be the only thing you leave the house with. So we’re not surprised by the popularity of digital wallets, as our study shows over two in five Americans are using digital wallets.

Traditionally, US banks have charged high fees for transferring money from your bank account to other people, but payment apps allow you to sidestep those fees by removing the bank as the middleman. For instance, major banks may charge up to $10 in next-day transfer fees, compared to one digital provider, Venmo, with one business day transfers not incurring any transaction fees.

While banks have been late to join the movement, media reports suggest they are no longer sitting on the sidelines. Many US banks, including Bank of America, Chase, Citi, and Wells Fargo, are planning to launch a payment app called Zelle reportedly next year.

The growth of digital wallet use in America is only a taste of the shake-up they are having on the banking payments market across the world. Research shows America ranks the lowest out of the top 20 countries for consumers preferring to use mobile payments over traditional wallet payments.”

To learn about Prove’s identity solutions and how to accelerate revenue while mitigating fraud, schedule a demo today.

The modern

way of proving identity

Trusted by 2500+ leading companies to reduce fraud and improve consumer

Keep reading

Read the article: Attackers Have Industrialized the Moment of Urgency: The Hidden Cost of OTP Nobody Talks About

Read the article: Attackers Have Industrialized the Moment of Urgency: The Hidden Cost of OTP Nobody Talks AboutDiscover the hidden costs of SMS OTPs, from fraud and failed delivery to customer abandonment, and how passkeys and persistent authentication reduce risk.

Read the article: How to Achieve More B2B Customer Growth With Prove Pre-Fill® for Business

Read the article: How to Achieve More B2B Customer Growth With Prove Pre-Fill® for BusinessProve Pre-Fill® for Business provides a comprehensive solution for organizations that want to onboard businesses by delivering faster onboarding, a decrease in abandonment, and a reduction in fraud (relative to attack rate).

Read the article: Account Takeovers: The Silent Revenue Killer

Read the article: Account Takeovers: The Silent Revenue KillerAccount takeover (ATO) fraud is rapidly becoming one of the biggest threats facing digital marketplaces and gig platforms. Learn how ATO attacks work, why they are accelerating, the latest fraud trends and statistics, and how continuous identity verification helps organizations prevent account takeovers while protecting revenue, customer trust, and user experience.

Trusted by 2,000+ leading companies to reduce fraud and improve consumer experiences, Prove is the world’s most accurate identity verification and authentication platform.